If Your ERP Profit Changes Overnight, Your Costing Method Might Be the Problem

If your ERP shows profit today and suddenly corrects it tomorrow, you are not alone.

Many businesses face:

- Sudden margin fluctuations

- Inventory value mismatches

- Confusion between purchase price and actual cost

And in most cases, the root cause is not ERP—it’s the wrong costing method.

After 18+ years of ERP implementation across industries, I’ve seen one common mistake:

Businesses apply a single costing method to all products without understanding how different product categories behave.

This blog will help you understand Weighted Average Purchase Order (PO) Costing, where it actually works, where it fails, and how to design costing correctly inside ERP.

What is Weighted Average Purchase Order Costing?

Weighted Average Purchase Order Costing calculates inventory cost using the purchase order price, even before the vendor invoice is posted.

In ERP systems, this is not a static formula—it is a dynamic moving average calculation that updates cost with every stock receipt.

Actual ERP Formula (Dynamic Moving Average)

This is the real engine running behind your ERP costing.

Why This Formula Matters in Real Business

Every time stock is received:

- Existing inventory value is recalculated

- New purchase value is added

- Cost becomes a rolling average

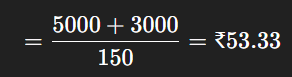

Example

Before Purchase:

- 100 units @ ₹50 → ₹5000

New Purchase:

- 50 units @ ₹60 → ₹3000

New Cost:

This new cost (₹53.33) is now used for:

- Sales

- Production consumption

- Inventory valuation

How to Know If Your ERP Costing is Wrong

You might already be facing costing issues if:

- Profit keeps fluctuating without business reason

- Inventory value doesn’t match actual purchase cost

- Frequent adjustments are required after invoice posting

- Finance and operations teams blame each other

If any of this sounds familiar, your costing design needs correction.

The Most Important Concept: Category-Based Costing

Here’s the reality from real ERP implementations:

No successful organization uses one costing method for all products.

Different product categories behave differently—and must be treated differently.

Product Categories and Recommended Costing

| Category | Nature | Recommended Costing | Why |

| Packing Material | Low value, local | Weighted Avg PO | Stable pricing |

| Raw Material (RM) | High value | FIFO / Avg Invoice | Accuracy critical |

| Semi-Finished (SFG) | Production stage | Standard Cost | Controlled costing |

| Finished Goods (FG) | Final output | Standard Cost | Stable pricing |

| Consumables | Indirect use | Weighted Avg PO | Simplicity |

Where Weighted Average PO Costing Works Best

✔ Packing Materials

- Cartons, labels, packaging

- Local procurement

- Minimal price variation

✔ Consumables

- Lubricants, maintenance items

- Low financial impact

In these categories, PO price ≈ Invoice price → minimal risk.

Where You Should NOT Use Weighted Avg PO

Avoid this method in:

- Import-heavy businesses

- Commodity trading (steel, chemicals)

- Industries with high price volatility

- Long procurement cycles

Because PO price ≠ actual cost.

Real-Life Example: When It Works Perfectly

Business:

FMCG company (carton purchases)

- PO1: 1000 units @ ₹10

- PO2: 2000 units @ ₹10.20

Average ≈ ₹10.13

Invoice difference: negligible

Result:

- Smooth costing

- No financial distortion

- Easy ERP management

Real-Life Example: When It Fails

Industry: Metal trading

Situation:

- PO price: ₹700/kg

- Invoice price: ₹750/kg

- Goods sold before invoice

What Happened:

- ERP used ₹700 as cost

- Sales showed higher profit

- Invoice posted later → cost increased

- Profit corrected downward

Impact:

- Margin instability

- Management confusion

- Loss of trust in ERP

Root cause: Wrong costing method for Raw Material.

The Costing Chain Impact (Critical Insight)

One wrong costing decision affects the entire business:

Wrong RM Cost

↓

Wrong Production Cost

↓

Wrong FG Cost

↓

Wrong Sales Margin

↓

Wrong Business Decisions

Why Raw Materials Should Avoid PO-Based Costing

Raw materials often include:

- Price fluctuations

- Freight & duties

- Currency changes

Using PO-based costing here leads to:

- Incorrect production cost

- Misleading margins

- Financial inconsistencies

Why SFG and FG Use Standard Costing

Semi-Finished and Finished Goods are manufactured, not purchased.

Their cost comes from:

- BOM

- Routing

- Overheads

Benefits of Standard Cost:

- Stable pricing

- Variance tracking

- Better planning and control

Hidden Consequences of Weighted Avg PO Costing

1. Profit Distortion

Profit looks higher initially, then corrects later

2. Inventory Misvaluation

Stock value differs from actual cost

3. Timing Dependency

Cost depends on transaction timing

4. Re-costing Complexity

ERP must adjust historical transactions

A Very Relatable Business Case

Business: Plastic manufacturer

Mistake:

Used Weighted Avg PO for all items

Result:

- Raw material cost incorrect

- Finished goods cost unstable

- Margins fluctuating

Fix:

- Packing → Weighted Avg PO

- RM → Weighted Avg Invoice

- FG → Standard Cost

Outcome:

- Stable financials

- Accurate costing

- Better decision-making

Practical ERP Implementation Approach

Step 1: Define Product Categories

RM, SFG, FG, Packing, Consumables

Step 2: Assign Costing Method

Category-wise—not random

Step 3: Configure Cost Flow

RM → Production → FG

Step 4: Enable Re-costing

Handle invoice differences

Step 5: Monitor Variances

PO vs Invoice, Standard vs Actual

How Cyprus ERP and Onfinity ERP Solve This

Most ERP systems fail because they treat costing as just a formula.

Cyprus ERP and Onfinity ERP approach it differently.

✔ Category-Based Costing Engine

Define costing method per product category

✔ Dynamic Moving Average Logic

Uses real-time Available + Incoming formula

✔ Multiple Costing Methods

- Weighted Avg PO

- Weighted Avg Invoice

- FIFO / LIFO

- Standard Cost

✔ Advanced Re-costing Engine

Handles:

- Backdated transactions

- Cost corrections

- High data volumes

✔ Full Manufacturing Cost Flow

RM → SFG → FG with BOM integration

The focus is simple:

Costing should reflect how your business actually operates—not just how the system calculates.

Final Thoughts

Weighted Average Purchase Order costing is powerful—but only when used correctly.

The real success lies in:

Using the right costing method for the right product category.

Key Takeaways

- Packing & Consumables → Weighted Avg PO ✔

- Raw Material → FIFO / Avg Invoice ✔

- SFG & FG → Standard Cost ✔

Need Help Designing Costing in Your ERP?

If you are facing:

- Incorrect inventory valuation

- Fluctuating margins

- Confusion between PO and Invoice cost

You are not alone—and this can be fixed.

We help businesses design category-based costing models that bring:

- Accuracy in financials

- Stability in margins

- Trust in ERP

Reach out for:

- Costing assessment

- ERP optimization

- Onfinity/Cyprus ERP demo

About the Author

Surya Sagar

Founder & ERP Solution Architect, BRS Infotek

With 18+ years of ERP implementation experience across global industries, Surya Sagar specializes in designing practical, scalable ERP solutions. He has contributed to platforms like Onfinity ERP (Formerly Vienna Advantage) and is the architect behind Cyprus ERP.

His expertise includes:

- ERP costing architecture

- Manufacturing & supply chain optimization

- Financial process automation

- High-volume ERP system design